(Screenshot)

Enrolling in Affordable Care Act coverage is looking a little bit different for 2023. So, here’s a breakdown of all the changes, and how to enroll for those that need coverage in Pennsylvania.

How to Enroll

Those interested in enrolling in Affordable Care Act coverage can do so now via Pennsylvania’s state-run exchange, Pennie, through Jan. 15, 2023. You must enroll by then to be eligible for 2023 coverage, unless you qualify for a Special Enrollment Period. You can also enroll by Dec. 15 for coverage that starts on Jan. 1, 2023.

To review plans and prices and enroll, click here.

Extended Subsidies to Help Afford Rising Premiums

Policies for 2023 are a bit more expensive than in previous years, but most enrollees won’t feel this increase due to enhanced federal subsidies first implemented as part of Joe Biden’s American Rescue Plan and later extended through this year’s Inflation Reduction Act.

The Affordable Care Act provided funding and basic parameters for states to establish their own exchanges, which Pennsylvania opted to do through Pennie. Pennie can lower an enrollee’s monthly premium and/or out-of-pocket costs in two ways: Advance Premium Tax Credits (APTC) and Cost-Sharing Reductions (CSR). For the former, when someone applies for coverage, they’ll estimate their expected income for 2023. If they qualify, they can use any amount of the credit in advance to lower their monthly payments. For the latter, if they qualify, an individual must enroll in a plan in the Silver category to get the extra savings.

Either way, the Biden administration’s newly-extended subsidies will allow 80% of enrollees to select plans that will cost less than $10 a month and will save these enrollees an average of $800 a year in premiums. Thanks to the Inflation Reduction Act, enrollees will also pay no more than 8.5% of their income on premiums, down from nearly 10%.

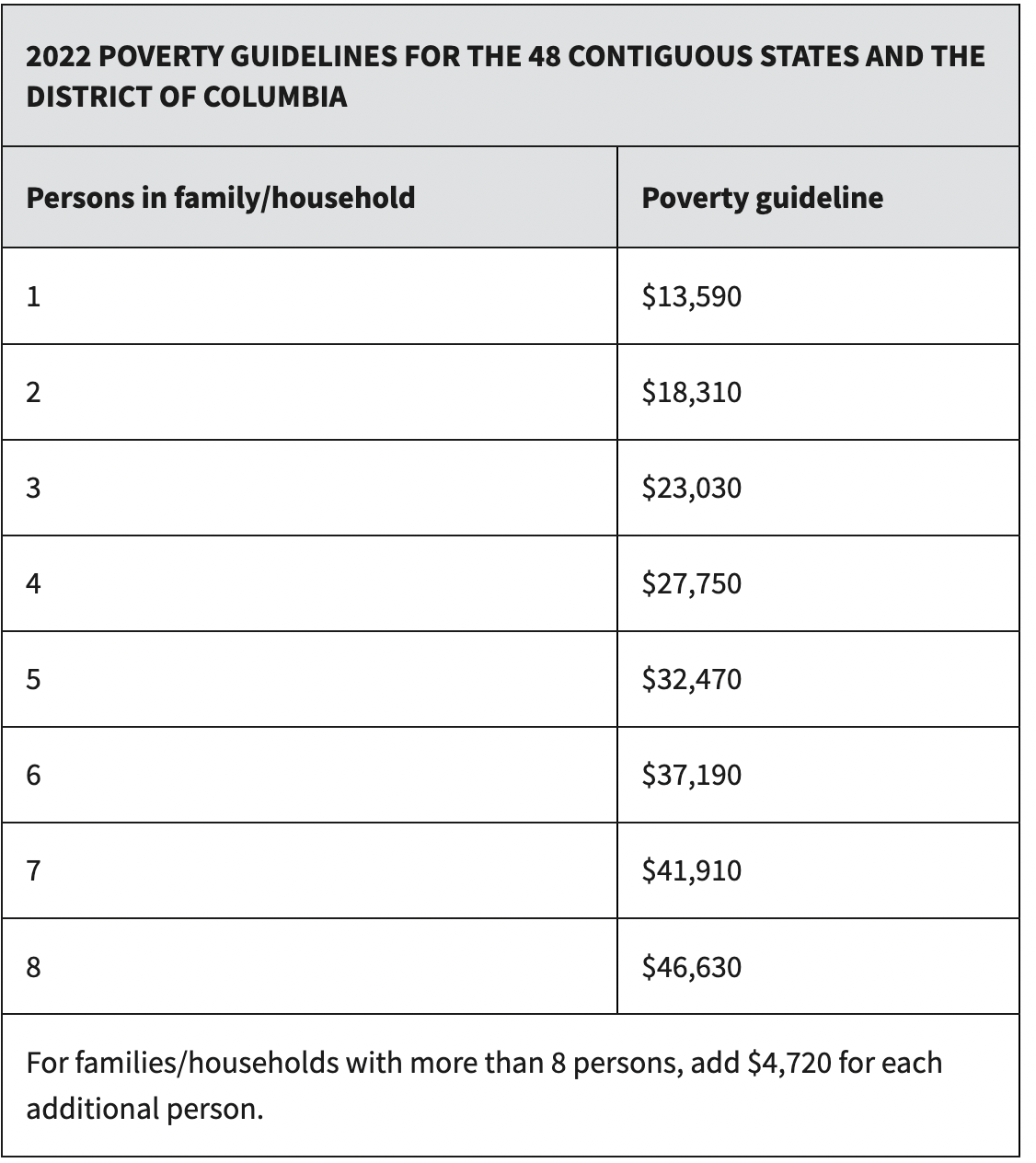

Lower income enrollees will have the opportunity to eliminate their premiums altogether by receiving these subsidies. And for the first time, those earning more than 400% of the federal poverty level—which is most Americans—are eligible for financial help.

More Choices on the Marketplace

Thirteen insurers are participating in the Pennie exchange in 2023 in Pennsylvania, the same number as in 2022.

Every carrier must also now offer a standardized plan at every metal plan level (Bronze, Silver, Gold, and Platinum), a change meant to simplify the insurance shopping experience. These plans will have a set deductible, out-of-pocket maximum, and copay or coinsurance, which will allow customers to more easily compare other elements of the plans offered, such as premium costs and provider networks. The deductibles for these standardized plans will be higher than in non-standardized policies, but certain benefits, such as primary care and urgent care, will be available pre-deductible.

No ‘family glitch’

Under the ACA, workers who aren’t offered “affordable” insurance coverage—a plan that costs them less than 10% of their income—by their employer are able to receive subsidies to purchase plans on the healthcare exchange. But until now, the ACA didn’t take into consideration how adding family members to employer-sponsored policies could push the cost above what families were able to afford. In these instances, workers and their families haven’t been eligible to get subsidies to buy ACA plans.

But thanks to a new Biden administration rule, family members of workers who are offered affordable individual plans by their employer but unaffordable family plans will be eligible for ACA subsidies in 2023.

About 1 million people nationwide will either gain coverage or see reductions in premiums, according to the White House.

Author

Politics

Malcolm Kenyatta makes history after winning primary for Pa. Auditor General

State Rep. Malcolm Kenyatta, who was first elected to the state House in 2018, won the Democratic nomination for Pa. Auditor General and will...

Biden administration bans noncompete clauses for workers

The Federal Trade Commission (FTC) voted on Tuesday to ban noncompete agreements—those pesky clauses that employers often force their workers to...

Philadelphia DA cancels arrest warrant for state Rep. Kevin Boyle on eve of Pa. primary

Philadelphia District Attorney Larry Krasner said a detective had sought the warrant against Boyle, a Democrat whose district includes a section of...

Local News

What do you know about Wawa? 7 fun facts about Pennsylvania’s beloved convenience store

Wawa has 60 years of Pennsylvania roots, and today the commonwealth’s largest private company has more than 1,000 locations along the east coast....

Conjoined twins from Berks County die at age 62

Conjoined twins Lori and George Schappell, who pursued separate careers, interests and relationships during lives that defied medical expectations,...