Tom, left, and Carol Shaw look over their healthcare research at their home in Lewisberry Township Feb. 9, 2026.

Tom and Carol Shaw are both 63. Tom is retired – he worked for 16 years for Capitol Blue Cross – and Carol teaches project management, part-time, at Harrisburg University. They live in a comfortable home on a cul-de-sac near Lewisberry, where they received the occasional visit from wild turkeys or songbirds who knock on the back door.

When Tom retired in August 2024, he kept the couple’s health insurance through COBRA, the law that allowed him to keep the coverage so long as he paid the full premium. In January 2025, he had to find new health coverage and went to Pennie, the health insurance exchange run by the state of Pennsylvania.

He shopped around – it was complicated – but was able to find coverage that compared favorably to the insurance he had from work. His experience with Blue Cross as a technical project manager gave him some insight. “I have more knowledge than the average person, but I still don’t get a lot of the behind-the-scenes stuff,” he said.

The couple’s new coverage would cost – with a subsidy from the federal government – $1,090 a month.

“We thought that was high,” Carol said.

But nothing prepared them for what they would face when they went to re-enroll in their insurance coverage for 2026.

For the same coverage – a policy that would cover Carol’s healthcare needs – the premium would jump to $3,505 a month, largely due to Congress allowing federal subsidies under the Affordable Care Act to expire. To put that in perspective, the average monthly mortgage payment in York County is about $1,300, according to the U.S. Census.

That’s a 221% increase.

As he began to shop around for more affordable insurance – even considering going without coverage for himself – Tom found that was “just the tip of the iceberg.”

Many simply drop coverage

The enrollment period for obtaining health insurance under the ACA ended Jan. 31, the state exchange extending the deadline a month to give those seeking coverage a chance to navigate the system rocked by massive increases in premium costs caused by the expiration of federal subsidies.

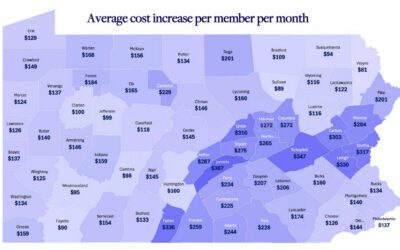

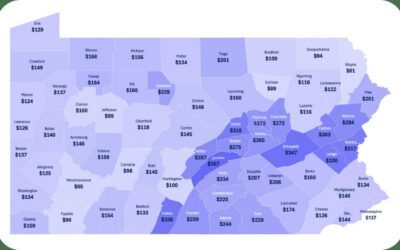

In Pennsylvania, according Pennie, premiums jumped on average 102 percent. The average premium increase in York County, according to Pennie, was 169 percent. The highest average was recorded in Juniata County, at 485 percent. The lowest, Sullivan County, with a population of fewer than 6,000 in the northeast corner of the state was 29 percent.

The increases prompted about 85,000 people to drop health insurance, according to figures released by Pennie Feb. 9, meaning that one in five enrollees terminated coverage. In York County, 3,655 of those previously covered by the ACA – 19 percent of those enrolled – dropped coverage. Before the premium increases took effect, Pennie reported it saw an increase in enrollment, but as the reality of higher premiums set in, more people decided to drop their coverage.

Pennie attributed the terminations to “adverse effects from unprecedented cost increases,” which “were a result of the expiration of enhanced premium tax credits that Congress did not extend.”

WellSpan Health had expected to see a drop in the number of patients insured through the ACA and reported it is “now seeing a decline.” The health care company is concerned that the reduction in the number of people with adequate insurance, or no insurance, will cause costs to increase. “People without insurance are less likely to seek care early for their conditions and often don’t access preventive care, resulting in later detection of health issues,” the company said in a statement. “Individuals who receive a diagnosis later in the course of an illness often have higher costs and longer recoveries.”

WellSpan helps uninsured patients to get insurance through the use of “presumptive eligibility” for Medicaid, which provides immediate, though temporary, coverage while an application for the government program is processed, the company said. It also has “a generous charity care policy” and offers financial assistance to patients struggling with costs. WellSpan spent $365 million in 2025 to assist uninsured and underinsured patients.

Premiums ‘the tip of the iceberg’

For those who were able to afford the premiums, the increase was only part of the equation.

When Tom Shaw was shopping for coverage, it became apparent that the choices weren’t terrific. Some plans included the couple’s primary physician or the orthopedist that Carol saw for her knee replacement. But they didn’t cover her cardiologist. Some of her prescription drugs were covered and others were not.

“It came down to having to choose between a bad option and a bad option, or multiple bad options,” he said. “A lot of people focused just on the premiums. But that’s just the tip of the iceberg.”

Costs associated with coverage were all higher. Previously, he said, they had a deductible of $1,650. The new coverage, a lesser plan that came with a monthly premium of $2,865, increased the deductible to $14,900, an 803 percent increase, Tom said. The maximum out-of-pocket expense went from $2,200 a year to $20,200. Co-pays jumped from $35 to $60 for doctor’s visits and from $45 to $85 for specialists. The emergency department co-pay doubled, from $150 to $300. Their cost for a medication Carol takes for her heart condition jumped from $23 a month to $1,000.

It was almost to the point that, Tom said, “what’s the point of having insurance at all? I feel we pay $2,800 a month for nothing.”

At one point, Tom, who is in good health, considered dropping his own coverage and just signing up Carol, but his wife nixed that idea. He looked into getting what’s called catastrophic coverage for himself, a bare-bones policy, but it was not available.

They felt they had no choice but to pay the higher premiums and absorb the higher costs. They still have a couple of years before they qualify for Medicare.

“We’re fortunate; we can afford it,” Carol said. “I really feel for people who can’t, people who have to make the choice between paying the rent and buying groceries or paying for health insurance. It has to be frustrating for people: Do I get food or do I get medicine?”

It has affected them, though. They had to take a hard look at their household budget and find places to cut expenses. “There were things we wanted to do in retirement,” Carol said. “We spent years saving for retirement to do some fun things. Now it’s all going for health care.”

Tom said, “It’s not what we had planned for our budget.”

“Or our retirement,” Carol said.

Author

Not all PA nursing homes share emergency plans. Did Bristol Rehab?

Before the deadly natural gas explosion at the Bristol Health & Rehab Center, the 174-bed nursing home had a plan, a series of protocols that...

Pa. pharmacists call on the state to take a bigger role in how they’re paid for Medicaid patients

Their plan would sideline middlemen in the pharmaceutical supply chain known as pharmacy benefit managers — or PBMs. As hundreds of pharmacies close...

More Pa. hospitals are creating private police forces to curb violence

Just spotting the word “police” on an officer’s badge can encourage people to keep their tempers in check or think twice about committing a crime,...

Gender-affirming health records from UPMC can’t be made anonymous, federal judge rules

U.S. District Judge Cathy Bissoon said the DOJ’s request carries a “stench” of ill-intent With a stinging rebuke of the credibility and motives of...

Mom’s ‘miracle’ baby defies odds after rare pregnancy rupture

Ericka Michel was standing on a stepstool in her Corry living room, spreading joint compound on drywall, when a small gush of fluid flowed between...